to leave a comment.

The battle for supremacy in the electric vehicle (EV) market is evolving beyond a simple 'vehicle sales volume' competition, transforming into a complex equation encompassing 'ecosystem dominance' across infrastructure, energy, and artificial intelligence (AI), as well as 'financial viability.'

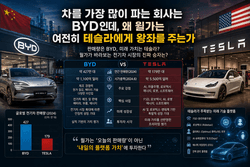

The EV market, once dominated by Tesla, now resembles the Three Kingdoms period, with China's BYD fiercely conquering roads worldwide and Rivian making a name for itself in the premium pickup truck market. However, from the perspective of the ruthless capital market—that is, the question of 'which stock deserves to claim the EV throne in 2026'—Wall Street still favors Tesla.

Behind Tesla's retention of the throne, even after losing the top spot in shipments, lies a profound context that is reshaping the paradigm of automotive manufacturing.

▲Photo: AI-generated image

BYD's Volume Hits a Great Wall: The 'U.S. Market' as the Missing Link

If the success or failure of the EV market were judged solely on 'production and sales volume,' the clear winner would be China's BYD. In 2025 alone, BYD sold a remarkable 4.6 million battery electric vehicles (BEVs) and plug-in hybrids (PHEVs) combined, achieving a 7.7% growth in external sales compared to the previous year.

Behind this explosive growth is a perfect 'Vertical Integration,' where BYD directly manufactures key components such as batteries, semiconductors, and electric motors. This has allowed BYD to achieve overwhelming cost control, which it has used to expand its territory into Europe, South America, and Southeast Asia, establishing itself as a global automotive powerhouse.

However, behind these impressive figures lies a critical limitation: the inability to enter the 'U.S. automotive market,' which is the world's second-largest and most profitable. Being blocked by America's strong trade and protectionist barriers from even observing a massive market of 16.4 million units annually is a weakness that cannot be lightly dismissed when evaluating long-term growth metrics.

As long as trade barriers remain, BYD's external growth risks being confined to price wars in limited territories, which is a decisive factor enabling Tesla to maintain its dominance in its home market (the U.S.) and secure financial flexibility.

The Cruel History of EVs Resembling a 'SaaS-pocalypse': Rivian's Profit Turnaround and Cash Burn Seesaw

U.S. startup Rivian is also writing a commendable and significant narrative. After years of severe losses, it finally achieved its first annual gross profit in 2025, demonstrating manufacturing efficiency. Annual revenue reached approximately $5.38 billion, and Rivian is currently gearing up for the launch of its mass-produced, low-cost SUV 'R2,' poised to change its fate.

However, a sober look at the books reveals that Rivian's estimated deliveries for this year are merely between 62,000 and 67,000 units. This is a tiny fraction of Tesla's production volume. Crucially, Rivian has still not escaped its company-wide net loss (deficit) structure.

In a macro environment of prolonged high interest rates and a contracting capital market, survival itself is a huge gamble for nascent EV companies that must burn through massive amounts of cash every quarter. Ultimately, Rivian's position, which relies solely on betting on future execution, stands in stark contrast to Tesla's overwhelming financial viability.

80,000 Charging Stations and the Megapack Empire: Tesla's 'Ecosystem' to Defend Against the Era of Zero Hardware Margins

Tesla's true formidable strength lies not merely in 'car sales.' Fierce price reduction competition has made margin compression an unavoidable reality across the EV industry, and Tesla is also experiencing a slowdown in delivery growth. However, Tesla has already built a robust platform ecosystem that can defend against a downturn where hardware sales margins approach zero.

Firstly, there's its global infrastructure dominance. Tesla operates over 80,000 'Supercharger' fast-charging stations worldwide, holding the key to the EV era's refueling supremacy. Secondly, the rise of its energy empire. The 'Megapack' large-scale energy storage business, which is penetrating the power grid utility market, has become a new core revenue stream for Tesla, riding on the trend of massive power infrastructure investment. Moreover, astronomical investments in Full Self-Driving (FSD), humanoid robotics, artificial intelligence (AI), and manufacturing automation create future pipelines that other companies dare not imitate.

Its financial firepower is also incomparable. Even amidst price wars, Tesla generated $6.2 billion in Free Cash Flow in 2025 alone, and as of the end of Q1 2026, it holds over $44 billion (approximately 60 trillion KRW) in cash and short-term investments on its books. This overwhelming war chest provides the flexibility to continue investing in securing future technological leadership without interruption, even during an EV slowdown.

The Victory of a Platform Company Beyond Automotive Manufacturing

The paradigm of EV competition has completely shifted. The race is no longer a pre-modern manufacturing battle of 'who can produce more cars.' It's a battle over who can more tightly control the artificial intelligence software ecosystem surrounding those cars, including charging infrastructure, energy storage, and extending to autonomous driving and robotics.

If BYD is the leader in quantitative growth, Rivian is a promising challenger. However, only one company has overcome all these challenges and completed an 'ecosystem' that generates its own cash flow: Tesla. This is precisely why Wall Street keeps the EV crown on Tesla, even after it conceded the shipment throne.

*Disclaimer: This article is for investment reference only, and we are not responsible for investment losses based on it. The content should be interpreted for informational purposes only.*

Newsletter

Get key news delivered to your email every morning

to leave a comment.